Search for insurance help

The Insurance Clock – What time is it?

Structural change and cost cycles are part of every industry, and Insurance is no different. The Insurance Clock above is a useful tool to represent where Insurance rates are right now and where they’re likely to be heading in the future.

Most agree the time is currently between 9 and 10 o’clock, which means not great news for you, the Policyholder.

With this hard market cycle, we will see:

- Period of higher premiums

- Getting insurance coverage could become more difficult and harder to negotiate terms

- Insurers reducing capacity to take on some risks or industry groups (e.g. recycling, financial services, directors/officers insurance)

- Higher excesses being requested

- More time required by your to place your insurance, often this will mean additional information is required from you

What has brought the insurance market to its current phase?

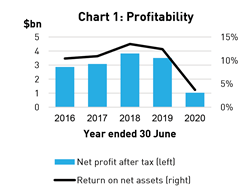

The recently released APRA (Australian Prudential Regulation Authority) June 2020 Quarterly Report showed insurance company profitability continuing to decrease, the chart below as of 30 June 2020

The chart highlights declining industry profitability for the 12-month period to 30 June 2020. This was due to the catastrophic bushfire and storm events of late December 2019 / early 2020, and the large falls in investment returns mainly attributable to the impact of CoV19 on investment markets and the continual cycle of low interest rates.

All underwriters are now experiencing shocks to every side of their financial statements, through deteriorating loss ratios on both short and long-tail insurance classes. The declining investment market has also had a significant impact on insurance industry profitability.

After a year of average market increases of around 6% – 8% for Commercial Insurance and 12%+ for large Property assets, the recently released APRA statistics indicate premiums will continue to rise in the vicinity of 9% – 12% for the next twelve months.

Of course, there are other market forces also at play, some of which are outlined below.

Low Interest Rates

Management Liability insurance is designed to provide protection to both the business and its directors or officers for claims of wrongful acts in the management of the business.

A business insurance pack can provide cover for your business premises and contents, against loss, damage, theft or financial loss from an insured interruption to the business.

Low Interest Rates

QUESTIONS? JUST ASK

Anthony Anastasio

A sustained period of low interest rates has had a significant impact on Insurers’ results. Whilst interest rates and investment returns are falling claims reserves need to be ‘topped up’.

Australian Dollar

The AU$ is now hovering around US73cents (September 2020). This has seen the continuation of claims cost inflation being higher than the general rate of inflation across the Australian economy. The impact has been particularly noticeable in repair costs of motor vehicles that rely on imported replacement parts and any building materials or equipment imported as part of a claims settlement.

Insurance Company Net Retentions

In the past decade or so the amount of losses held locally by insurance companies has increased. This means many smaller weather events, for example, aren’t falling into reinsurance treaties – and local companies are picking up the losses to their net account.

Looking to the Future

We therefore recommend preparing early for your renewal; and consider partnering with Everest Risk Group.

In this environment, it’s crucial we work together to maintain policy terms and conditions even though prices are on the increase. After all, as our experience shows us time and time again, price is ultimately forgotten when an insurable loss happens.

General Advice Warning: This advice is general and does not take into account your objectives, financial situation or needs. You should consider whether the advice is appropriate for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement.

All information above has been provided by the author.

All information above has been provided by the author.

Anthony Anastasio, Everest Risk Group Pty Ltd, ABN 97 106 984 623, AFSL 240549

This article originally appeared on Everest Risk Group News and has been published here with permission.

QUESTIONS? JUST ASK

Anthony Anastasio

Comments (0)

Related articles

Related insurance brokers

16 reviews

Featured

Featured

a day

58 reviews

Featured

a few hours

6 reviews

a few minutes