Search for insurance help

What You Need to Know About Insurer Profitability

The COVID-19 pandemic has hit many industries hard. While Australia has managed to avoid sharper contractions in GDP compared to countries like France and the UK, Federal Treasurer Josh Frydenberg has said Australia’s economy is predicted to be around 6% smaller by the end of 2020/21 than the previous year.

While many industries have taken a hit, a notorious year of natural disasters, weather perils and unsteady global financial markets mean that profitability for insurers in Australia is the worst in 20 years. A new industry Optima report by the actuarial firm Finity shows that return on equity (ROE) for insurers has dropped to 4%, down from 13% in the 12 months prior. What’s more, these figures do not represent the full impact of the COVID-19 pandemic which is yet to surface.

These market conditions are leading to something called a ‘hard’ insurance market or ‘firming of rates’, and this is something that insurance customers should be prepared for.

What is a hard insurance market?

In the insurance industry, a ‘hard market’ refers to changes in the market that lead to an increase in insurance premiums and a decreased capacity for most coverage. In contrast, a soft market is when the industry sees low premium rates, flexible contracts and high coverage availability.

What does this hard market mean for insurance customers?

For insurance customers, hard market conditions mean less competition by insurers for their business, as insurers exit unprofitable market segments. This decrease in competition leads to increasing insurance premiums and increases in excesses. For new businesses, those with an adverse claims history or who require a policy to be modified from standard, the premium will be the highest, with some businesses potentially being unable to find cover.

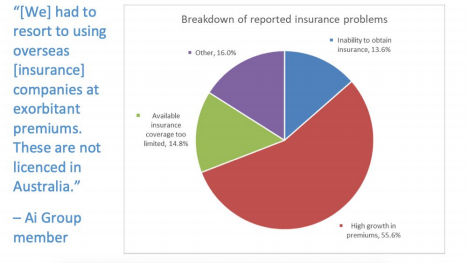

According to a recent survey by The Australian Industry Group, 53% of businesses polled have experienced problems seeking insurance, with 55.6% of these businesses reporting the biggest problem to be high growth in premiums. The second biggest problem was ‘other’ (16%), which the majority of businesses reported as a lack of competition and rates to choose from.

Image source: The Australian Industry Group Business Insurance Report: Unaffordable or Unavailable, October 2020

Insurance HQ is committed to providing the most comprehensive cover at affordable rates. We will endeavour to update our customers as and when the situation changes, but please get in touch if you have any questions or concerns. Our team of brokers will be more than happy to have a chat.

Management Liability insurance is designed to provide protection to both the business and its directors or officers for claims of wrongful acts in the management of the business.

A business insurance pack can provide cover for your business premises and contents, against loss, damage, theft or financial loss from an insured interruption to the business.

Insurance HQ is committed to providing the most comprehensive cover at affordable rates. We will endeavour to update our customers as and when the situation changes, but please get in touch if you have any questions or concerns. Our team of brokers will be more than happy to have a chat.

QUESTIONS? JUST ASK

Adam Pile

General Advice Warning: This advice is general and does not take into account your objectives, financial situation or needs. You should consider whether the advice is appropriate for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement.

All information above has been provided by the author.

All information above has been provided by the author.

Adam Pile, Insurance HQ Pty Ltd, ABN 33606759228, AFSL 363610

Related articles

QUESTIONS? JUST ASK

Adam Pile

Comments (0)

Related articles

Related insurance brokers

16 reviews

Featured

Featured

a day

58 reviews

Featured

a few hours

2 reviews